Would you have as much faith in your guidance counselor’s recommendation to attend a college if she received a $5,000 kickback from that college for every student she convinced to matriculate? Would you be more likely to buy a car if, instead of dealing with Johnny the Car Salesman, you were having a conversation about your vehicular future with Jonathan, Automobile Adviser, CAA, MCS? (For the purposes of this hypothetical CAA and MCS are meaningless acronyms I made up for “Certified Auto Adviser” and “Master Car Salesman,” bear with me.)

A Changing Landscape

The landscape for financial advice is mired in conflicts of interest and an alphabet soup of titles that on the surface convey impartiality and inspire trust, like Jonathan and our hypothetical guidance counselor. But for years, financial wolves have been cloaked in trusted adviser clothing – masking their real status as self-interested brokers who don’t have your best interest in mind. According to a recent report by the White House Council of Economic Advisers, these salespeople are fleecing hard-working Americans out of $17 billion in retirement funds each year.

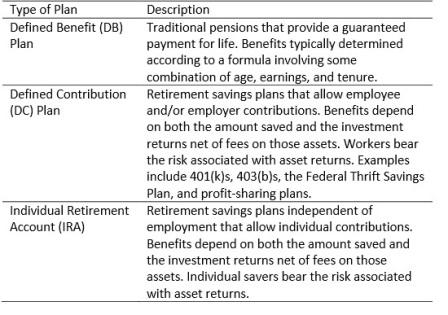

The transition in the American economy from guaranteed pensions to individual retirement accounts has resulted in a fundamental shift in risk from employers to employees. This shift has required individuals to become increasingly responsible for their own retirement funds. Personal finance pundits, employers, and even the government have focused significant attention on nudging individuals to start saving for retirement early and take advantage of the time value of money. Techniques, such as automatically enrolling individuals in a retirement account when they are hired (with the option to opt-out) have reduced the power of inertia and complexity that had prevented many from taking important step towards saving for retirement. While this is a necessary component, it is not sufficient.

White House Council of Economic Advisers Report: The Effects of Conflicted Advice on Retirement Savings

Ensuring that Americans are getting the best advice to manage the money they are socking away has not received adequate attention. This is especially true as people today tend to hop between jobs more frequently. When trying to consolidate their retirement savings, many undertake a process known as a rollover in which they move large retirement sums from an employer-sponsored plan, like a 401(k), to an Individual Retirement Account (IRA).

Investors are particularly vulnerable to conflicted advice when it comes to the market for Individual Retirement Accounts (IRAs) and rollovers. As the White House report indicated, more than 40 million American families have savings of more than $7 trillion in IRAs. Rollovers to IRAs exceeded $300 billion in 2012.

Often, an individual rolling savings over from a 401(k) to an IRA is making a decision about a substantial sum of money and is faced with a staggering array of investment options. Crucially, unlike a company pension managed by experienced investment professionals, “typical investors are often not sophisticated enough to spot the pitfalls and may fall victim to sales tactics disguised as earnest financial advice” when deciding about how to allocate funds in an IRA, according to a Boston Globe article.

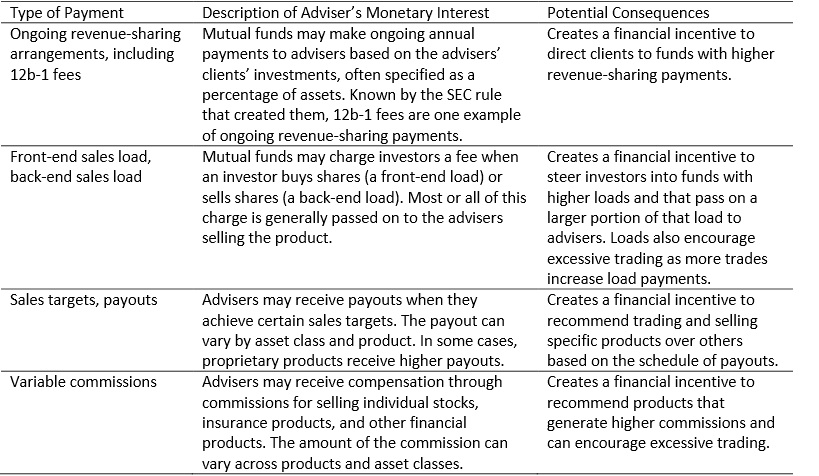

Thus, it is natural that many turn to “professional” advice. The menu of advisers runs the gamut in terms of titles and credentials, but differs along two key dimensions: the legal standard their advice must meet and how they are compensated for the advice they provide. Many financial advisers are compensated through fees and commissions that depend on their clients’ actions. For example, if a client buys shares in certain mutual funds, the broker may receive a commission, known as a front-end sales load, from the mutual fund company. Or an adviser may receive a bonus from his employer for reaching sales targets on certain products, typically proprietary ones on which the employer is profiting. A broker is thus incentivized to steer clients towards these funds over other products that may be identical, but are lower in cost. According to the White House report, “such fee structures generate acute conflicts of interest: the best recommendation for the saver may not be the best recommendation for the adviser’s bottom line.”

White House Council of Economic Advisers Report: The Effects of Conflicted Advice on Retirement Savings

“The client must be king”

The most prudent way to protect consumers would be to ensure that all advisers are required by law to put their consumer’s interest first and, therefore, above their own, what’s known as a fiduciary duty.

“Fiduciary duty is the highest duty known to the law,” John Bogle, the founder of investment management company Vanguard, wrote in “The Fiduciary Principle: No Man Can Serve Two Masters.” It ensures that “the client. . . must be king.”

Why would you want to take advice from someone who doesn’t have your best interest at heart? While some sources of investment advice, like Registered Investment Advisers (RIAs) do have a fiduciary duty, many others, like broker-dealers, do not.

This distinction may sound trivial, but is crucially important. Starkly put, brokers are able to recommend sub-optimal investments that are not in the best interest of their client. Such recommendations are legal as long as they are “suitable”, a loose term that means brokers have considered a client’s financial needs, objectives and unique circumstances. Brokers can give “suitable” advice, even if this means saddling the investor with higher cost funds that, not so coincidentally, put more and more money in the broker’s pocket.

The suitability standard leaves a lot of room for brokers to benefit themselves by making recommendations on which they earn hefty fees. “They can’t put your grandma in a heavy tech fund, but they could put her in a more expensive bond fund that pays them a huge commission,” said Kent Smetters, Professor of Business Economics and Public Policy at Wharton.

A Few Bad Apples or a Rotten Barrel?

The problem stems from the fact that those giving advice about IRAs and rollovers fall into the “suitable” rather than fiduciary category, unbeknownst to many consumers.

It would be wrong to indict the entire investment professional community as there are many assiduous advisers who have helped millions of Americans properly save for retirement; however, it would also be naive to assume that conflicted advice problems are confined to a few bad apples.

One revealing study titled, “The Market for Financial Advice: An Audit Study,” found systemic failures and “advisers [that] fail to de-bias their clients and often reinforce biases that are in their interests.” Economists Sendhil Mullainathan, Markus Noeth, and Antoinette Schoar sent mystery shoppers, posing as middle-class investors, to ask retail brokers for investment advice. Only 21 of 284 brokers recommended investing in index funds, while close to half steered clients toward actively managed mutual funds.

However, study after study has shown “that most active managers fall short of their benchmarks because of the higher fees, trading costs, and timing errors associated with frequent trading.” As Morningstar summarizes, “if there’s anything in the whole world of mutual funds that you can take to the bank, it’s that expense ratios help you make a better decision. In every single time period and data point tested, low-cost funds beat high-cost funds.” In other words, advisors should generally be recommending low-cost index funds not high-cost actively managed ones.

“Advisers encourage returns-chasing behavior and push for actively managed funds that have higher fees, even if the client starts with a well-diversified, low-fee portfolio,” the researchers wrote.

Yudesign | Dreamstime.com

Simply put, conflicted advice leads to lower investment returns. The Council of Economic Advisers scathing report quantified the losses at $17 billion annually. Even worse,the report found that “a retiree who receives conflicted advice when rolling over a 401(k) balance to an IRA at retirement will lose an estimated 12 percent of the value of his or her savings if drawn down over 30 years.”

Moving Towards Solutions

Earlier this year, the Labor Department resurrected its proposal from 2011 that would require brokers to act as fiduciaries. This rule would help ensure the financial security of hard-working Americans. It is a testament to the sheer power of the financial services lobbying army – comprised of banks with brokerage arms, insurance companies who sell annuities, “mutual fund companies that thrive on clients who roll their 401(k) plans into IRAs” and independent brokers and financial planners – that has kept this rule from being adopted for over four years. Arguments range from fear-mongering – a fiduciary requirement on brokers would throw the whole retirement system into chaos – to specious – excessive restrictions would make it economically unfeasible to offer financial advice at the lower end of the market. All seem designed to obfuscate the issue and provide air cover for the real goal: maintaining higher profits for brokers, even at the expense of the people they are meant to advise.

In an article on the intense lobbying efforts against the fiduciary rule, Eduardo Porter highlights the underlying issue for Wall Street. David Swensen, who manages Yale University’s investment portfolio, told Porter that “Wall Street makes no money on low-cost index funds.” Furthermore, Porter cites a report by the Government Accountability Office of Congress, which found that advisers were handsomely compensated, to the tune of $6,000 to $9,000, if clients rolled their savings from 401(k) plans to IRAs.”

Brokers may be incensed by the prospect of a fiduciary requirement because they are afraid of having to create a merit based business model in which their profits are correlated with the quality of their recommendations. It’s clearly more profitable for brokers to keep the current system where they “act opportunistically to the detriment of their clients.” Through this lens, it is easy to see why financial lobbyists are trying to maintain the status quo in which a weaker standard allows brokers to receive kickbacks from mutual funds for recommending sub-optimal, “suitable” investments.

The Regulation, Innovation, and Education Triumvirate

Ensuring financial security is a combination of regulation, product innovation, and education. While the Obama administration is busy fighting, and hopefully winning, on the regulation front, individuals and businesses must also take matters into their own hands.

On the product innovation side, we are already seeing a burgeoning revolution in the world of financial technology (known as “fintech”). With companies like Wealthfront and Betterment leading the way, there is momentum and a model for low-cost, automated advising. To argue that a fiduciary rule would make it economically unfeasible to offer advice at the lower end of the market ignores this momentum and underestimates innovation and American capitalism. Just think about the ventures that could have been seeded if, instead of giving lobbyists millions of dollars to preserve the status quo and fight the Labor Department rule, Wall Street had invested in funding creative solutions?

In addition to regulation and product innovation, Americans should educate and protect themselves from being duped by conflicted advice. Remember that you, as the client, are king, and that brokers work for you. You should interview and vet anyone before trusting them with your retirement dollars and financial security. The New York Times’ financial columnist, Tara Siegal Bernard, suggests that consumers ask a prospective adviser to sign an oath stating they will act as fiduciaries. Bernard writes that the oath, according to securities lawyer Andrew Stoltmann, would be binding in arbitration, which is important because most disputes between clients and financial advisers are settled in this forum.

The request for an oath could also help settle the question: fiduciary or douche. If an adviser won’t sign, then he’s definitely not the former.